Tips on how to cut up RRIF revenue with a partner to get the $2,000 tax credit score

For the general public, it is sensible to transform sufficient of your RRSP to a RRIF and declare the pension tax credit score

Opinions and proposals are independent and merchandise are independently decided on. Postmedia might earn an associate fee from purchases made thru hyperlinks in this web page.

Article content material

Via Julie Cazzin with Allan Norman

Commercial 2

Article content material

Q: I simply grew to become 65 years of age and nonetheless paintings complete time. To profit from the $2,000 pension tax credit score, I want to convert a minimum of a few of my registered retirement financial savings plan (RRSP) right into a registered retirement revenue fund (RRIF) in order that I will be able to withdraw $2,000 every December as qualifying pension revenue. My query is, if I set this up lately, can I withdraw the $2,000 and declare it as qualifying pension revenue for 2023? Additionally, my spouse Dorothy is 63 years previous. Can RRIF pension revenue be cut up together with her? Or does she want to be 65 years of age? What’s one of the simplest ways for me to profit from this tax credit score for my spouse and I at this level? — James S.

Article content material

FP Solutions: James, that’s a just right query. I in finding there may be some confusion across the pension tax credit score. Numerous other people suppose they will have to mechanically convert all or a few of their RRSP to a RRIF and draw $2,000 consistent with yr to assert the pension tax credit score when they input the yr they flip 65. Some other people even suppose claiming the pension tax credit score is a approach to get $2,000 out in their RRSP/RRIF tax loose. Neither of those ideas are essentially right kind. Let me briefly cope with your questions after which I’ll dive just a little deeper into the pension tax credit score.

Article content material

Commercial 3

Article content material

You’re proper, within the yr you flip 65, you’ll declare the federal $2,000 pension tax credit score despite the fact that you might be nonetheless operating. There’s a record of what qualifies as pension revenue, and RRIF revenue qualifies, which is the explanation you need to transform a few of your RRSP to a RRIF. I presume you aren’t changing your entire RRSP holdings to a RRIF, since the minimal RRIF withdrawals will power you to attract greater than $2,000 consistent with yr out of your RRIF, which is greater than what you’ll declare for the pension tax credit score.

Your RRIF revenue can also be cut up along with your spouse within the yr you flip 65 despite the fact that Dorothy isn’t but 65. The pension tax credit score is non-refundable, that means you’ll’t cut back your revenue beneath 0 and be expecting to get a tax refund — it’s non-refundable. You’ll be able to, on the other hand, switch all, or the unused portion, of the pension tax credit score in your spouse.

Commercial 4

Article content material

Sadly for you, James, your spouse will have to be 65 on this case. Curiously, there are qualifying pensions that do permit you to switch the pension tax credit score to a partner below the age of 65, however RRIF revenue isn’t considered one of them.

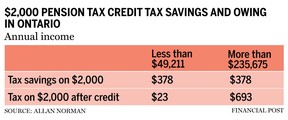

Now, the query is will have to you exchange a few of your RRSP to a RRIF and declare the pension tax credit score? In Ontario, the tax financial savings is $378 regardless of your tax bracket, excessive or low, which you’ll see within the accompanying desk, at the side of the tax owing.

As you’ll see, there may be little or no tax owing on the decrease revenue stage when the mixed federal and Ontario tax fee — 15 consistent with cent and 5.05 consistent with cent, respectively — is 20.05 consistent with cent. The federal pension tax credit score is calculated as 15 consistent with cent of $2,000, or $300, which offsets the $300 of federal tax owing. In Ontario, the pension tax credit score solely applies to pension revenue as much as $1,541, leading to a credit score of $78 (or 5.05 consistent with cent of $1,541). You continue to need to pay provincial tax at the ultimate $459 at 5.05 consistent with cent, which involves $23.

Commercial 5

Article content material

The similar applies to other people incomes greater than $235,675 consistent with yr, the absolute best tax bracket in Ontario, however the mixed federal and provincial tax fee is 53.53 consistent with cent, so high-income earners must pay some federal and provincial tax at the $2,000 RRIF withdrawal.

James, I’m no longer positive what your present revenue is or how lengthy you propose to stay operating. No query, there are tax financial savings for you right here. If I used to be to complicate this and search for causes so that you can no longer convert a portion of your RRSP to a RRIF, listed here are 3 of them:

Will you be in a decrease tax bracket and pay much less tax at the $2,000 RRIF withdrawal whilst you forestall operating?

Are you higher to go away the $2,000 for your RRSP so the investments compound tax sheltered till you flip 72?

Commercial 6

Article content material

Will there be an extra account commission when you open a RRIF account?

Thankfully, it doesn’t should be that difficult with regards to the pension tax credit score. There’s a small tax financial savings, and also you aren’t going to make a significant mistake regardless of your choice, so cross along with your intestine. For the general public older than 65 with out pension revenue, it is sensible to transform sufficient of your RRSP to a RRIF and declare the pension tax credit score.

Allan Norman supplies fee-only qualified monetary making plans products and services thru Atlantis Monetary Inc. and offers funding advisory products and services thru Aligned Capital Companions Inc., which is regulated through the Funding Trade Regulatory Group of Canada. Allan can also be reached at alnorman@atlantisfinancial.ca

Feedback

Postmedia is dedicated to keeping up a full of life however civil discussion board for dialogue and inspire all readers to proportion their perspectives on our articles. Feedback might take as much as an hour for moderation ahead of showing at the website online. We ask you to stay your feedback related and respectful. We have now enabled e-mail notifications—you’ll now obtain an e-mail when you obtain a answer in your remark, there may be an replace to a remark thread you practice or if a person you practice feedback. Consult with our Neighborhood Tips for more info and main points on find out how to alter your e-mail settings.

Sign up for the Dialog