Break up-12 months Backdoor Roth IRA in FreeTaxUSA, second 12 months

The former publish Break up-12 months Backdoor Roth IRA in FreeTaxUSA, 1st 12 months handled contributing to a Conventional IRA for the former 12 months and recharacterizing a prior 12 months’s Roth IRA contribution as a Conventional IRA contribution. This publish handles the conversion phase in FreeTaxUSA.

We duvet two instance situations on this publish. Right here’s the primary:

You contributed $6,000 to a Conventional IRA for 2022 in 2023. The worth higher to $6,200 whilst you transformed it to Roth in 2023. You gained a 1099-R shape record this $6,200 Roth conversion.

You will have to’ve already reported the contribution phase in your 2022 tax go back by way of following Break up-12 months Backdoor Roth IRA in FreeTaxUSA, 1st 12 months. The IRA custodian despatched you a 1099-R shape for the conversion in 2023. This publish displays you put it into FreeTaxUSA.

Right here’s the second one instance state of affairs:

You contributed $6,000 to a Roth IRA for 2022 in 2022. You discovered that your source of revenue used to be too top whilst you did your 2022 taxes in 2023. You recharacterized the Roth contribution for 2022 as a Conventional contribution sooner than April 15, 2023. The IRA custodian moved $6,100 out of your Roth IRA in your Conventional IRA as a result of your authentic $6,000 contribution had some profits. The worth higher once more to $6,200 whilst you transformed it to Roth in 2023. You gained two 1099-R bureaucracy, one for $6,100 and some other for $6,200.

You will have to’ve already reported the recharacterized contribution in your 2022 tax go back by way of following Break up-12 months Backdoor Roth IRA in FreeTaxUSA, 1st 12 months. The IRA custodian despatched you two 1099-R bureaucracy, one for the recharacterization, and the opposite for the conversion. This publish displays you put either one of them into FreeTaxUSA.

If you happen to contributed for 2023 in 2024 or for those who recharacterized a 2023 contribution in 2024, you’re nonetheless within the first 12 months of this adventure. Please stick to Break up-12 months Backdoor Roth IRA in FreeTaxUSA, 1st 12 months. If you happen to recharacterized your 2023 contribution in 2023 and transformed in 2023, please use a unique follow-up publish.

If neither of those instance situations suits you, please seek the advice of our information for a standard “blank” backdoor Roth: Learn how to Document Backdoor Roth In FreeTaxUSA (Up to date).

If you happen to’re married and each you and your partner did the similar factor, you will have to stick to the stairs under for each your self and your partner.

1099-R for Recharacterization

This segment best applies to the second one instance state of affairs. If you happen to contributed immediately to a Conventional IRA for the former 12 months and didn’t recharacterize (the primary instance state of affairs), please skip this segment and soar over to the conversion segment.

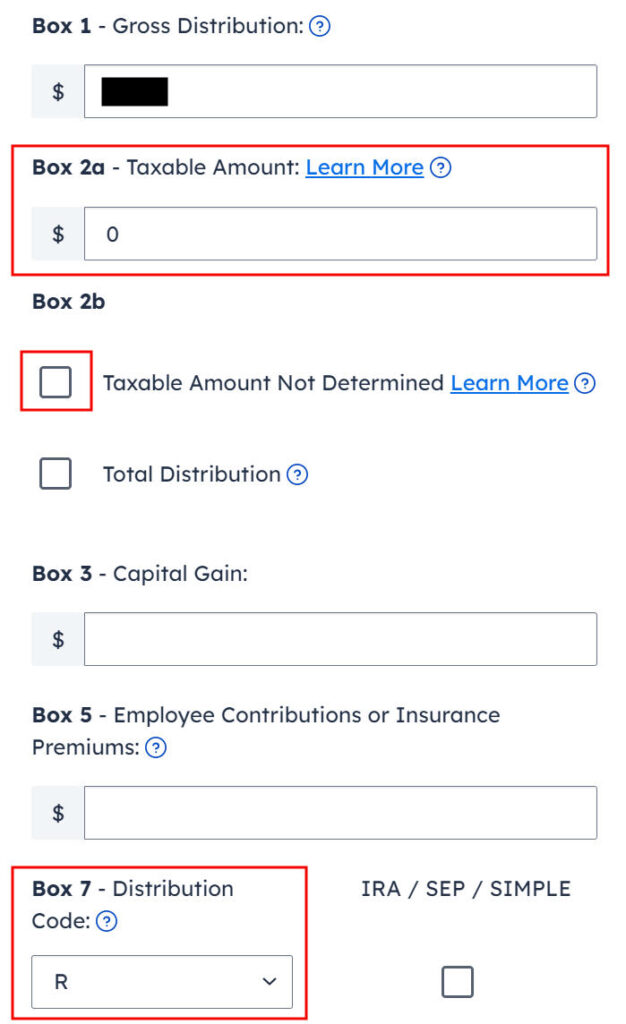

We take care of the 1099-R shape for recharacterization first. This 1099-R shape has a code “R” in Field 7.

To find “Retirement Source of revenue (1099-R)” below the Source of revenue menu.

Click on at the “Upload a 1099-R” button.

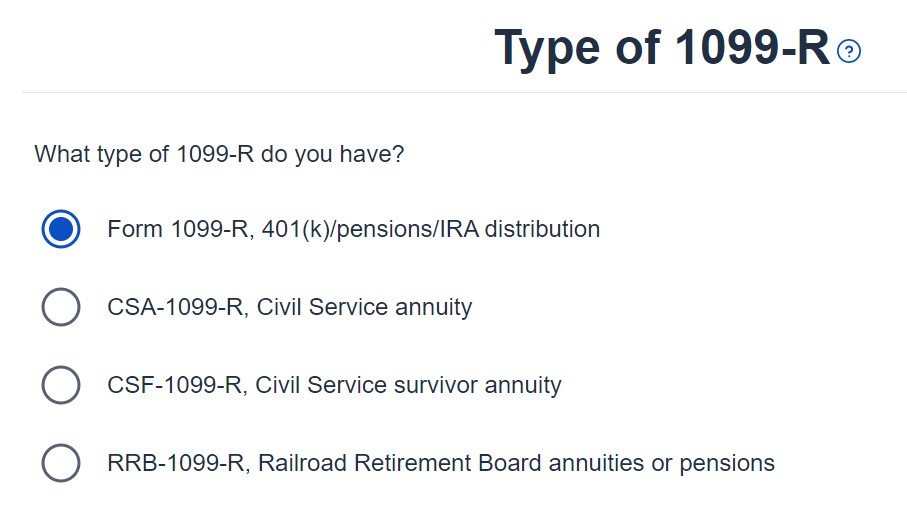

It’s simply a normal 1099-R.

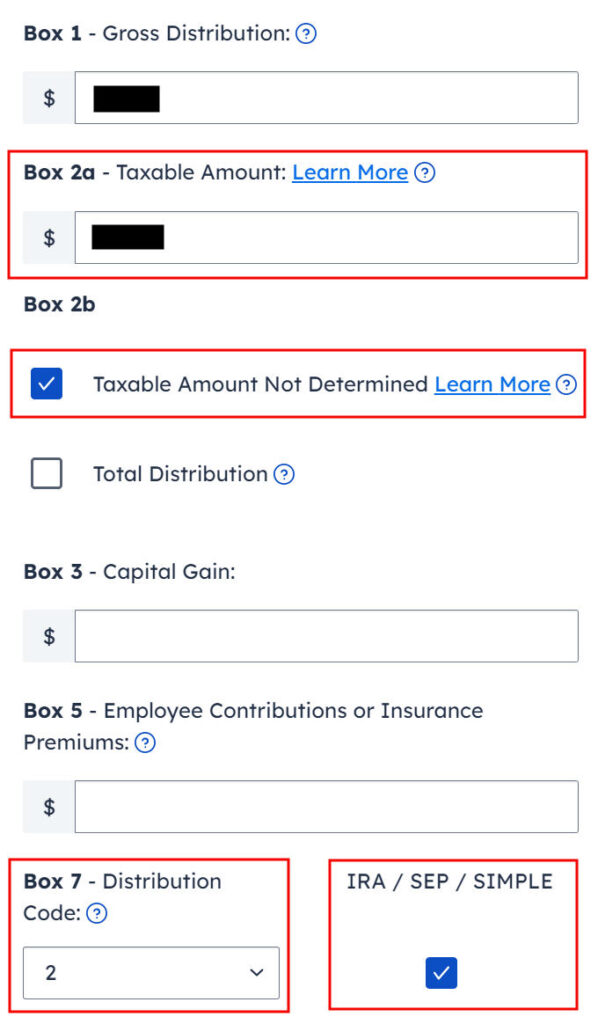

Input the 1099-R for the recharacterization precisely as you may have it. Field 1 displays the volume that used to be transferred from the Roth IRA to the Conventional IRA whilst you recharacterized your 2022 contribution. Field 2a displays that the recharacterization isn’t taxable. Field 2b “taxable quantity now not made up our minds” isn’t checked. The code in Field 7 is “R.” The “IRA / SEP / SIMPLE” field isn’t checked.

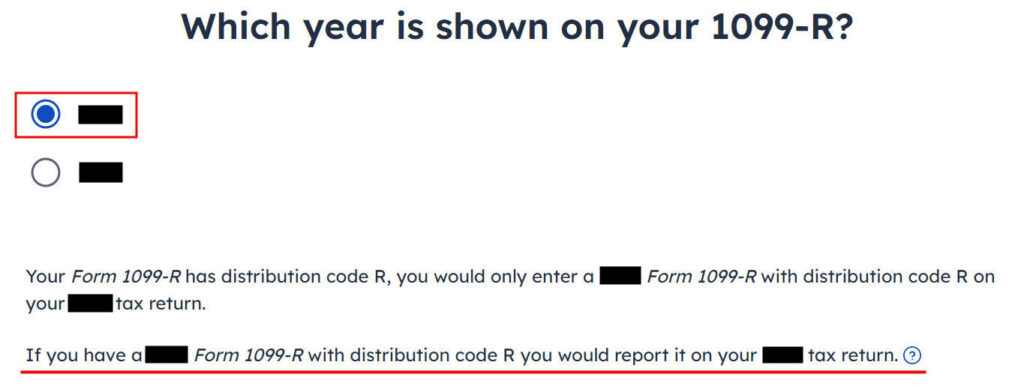

Your 1099-R displays 2023 however FreeTaxUSA says you will have to’ve reported it in your 2022 tax go back. The issue is you didn’t have it again then. You couldn’t have reported one thing you didn’t have. Make a selection the proper 12 months and proceed anyway.

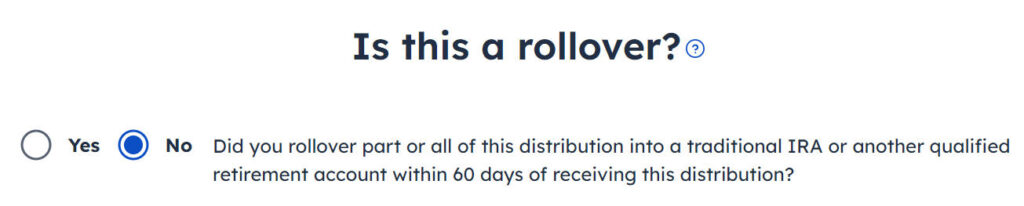

The recharacterization wasn’t a rollover.

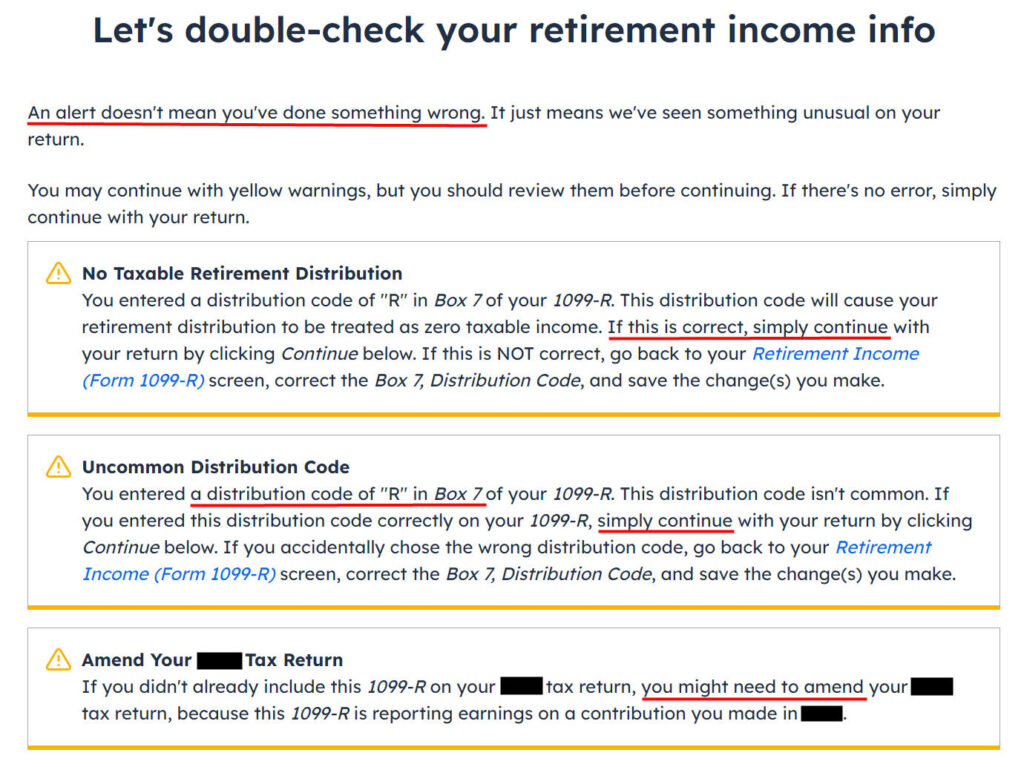

FreeTaxUSA displays some signals. The 0 taxable source of revenue at the 1099-R is proper. Code “R” in Field 7 may be proper. Despite the fact that you didn’t come with this 1099-R ultimate 12 months since you didn’t have it at the moment, you don’t want to amend ultimate 12 months’s tax go back for those who reported the recharacterization otherwise whilst you adopted Break up-12 months Backdoor Roth IRA in FreeTaxUSA, 1st 12 months. You might want to amend ultimate 12 months’s go back provided that you didn’t file the recharacterization ultimate 12 months in any respect.

You’re achieved with the 1099-R shape for the recharacterization. Click on at the “Upload a 1099-R” button so as to add the opposite 1099-R for the conversion.

1099-R for Conversion

The 1099-R for conversion has a code “2” in Field 7 for those who’re below age 59-1/2 or a code “7” for those who’re 59-1/2 or older.

It’s additionally a normal 1099-R.

Field 1 displays the volume transformed to Roth. If you happen to contributed to a Conventional IRA for 2023 in 2023 and transformed in 2023 (a “blank” backdoor Roth) on most sensible of changing the 2022 contribution in 2023, the volume at the 1099-R comprises two years’ value of contributions. It’s commonplace to have an identical quantity because the taxable quantity in Field 2a when Field 2b is checked pronouncing “taxable quantity now not made up our minds.” Be certain that to select the proper code in Field 7 to check your 1099-R. The “IRA / SEP / SIMPLE” field is checked.

Your refund quantity drops after you input the 1099-R. Don’t panic. It’s commonplace and transient. The refund quantity will arise after we end the entirety.

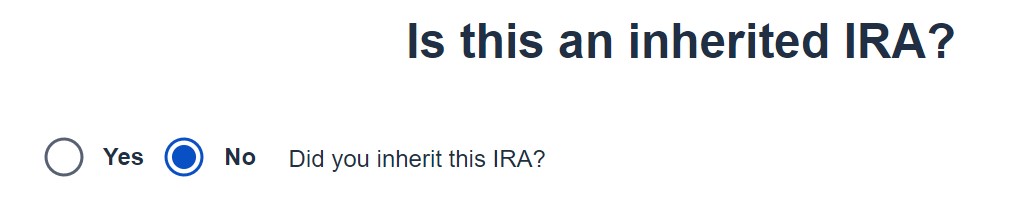

It’s now not an inherited IRA.

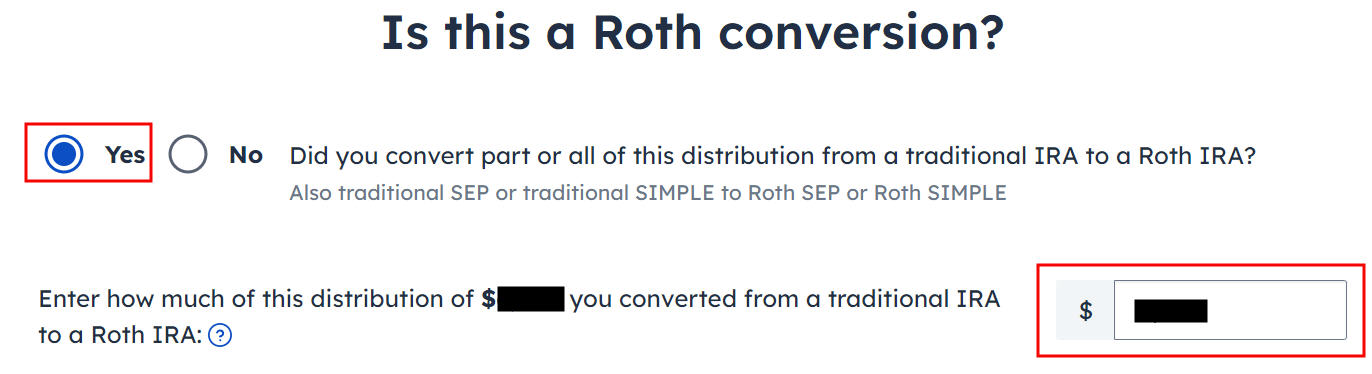

It’s a Roth conversion. 100% of the volume at the 1099-R used to be transformed from a Conventional IRA to a Roth IRA.

You might be achieved with this 1099-R for the conversion. Repeat you probably have some other 1099-R. If you happen to’re married and either one of you transformed to Roth, be aware of whose 1099-R it’s whilst you input the second. You’ll have issues for those who assign each 1099-R bureaucracy to the similar particular person once they belong to each and every partner. Click on on “No, Proceed” in case you have entered the entire 1099-R bureaucracy.

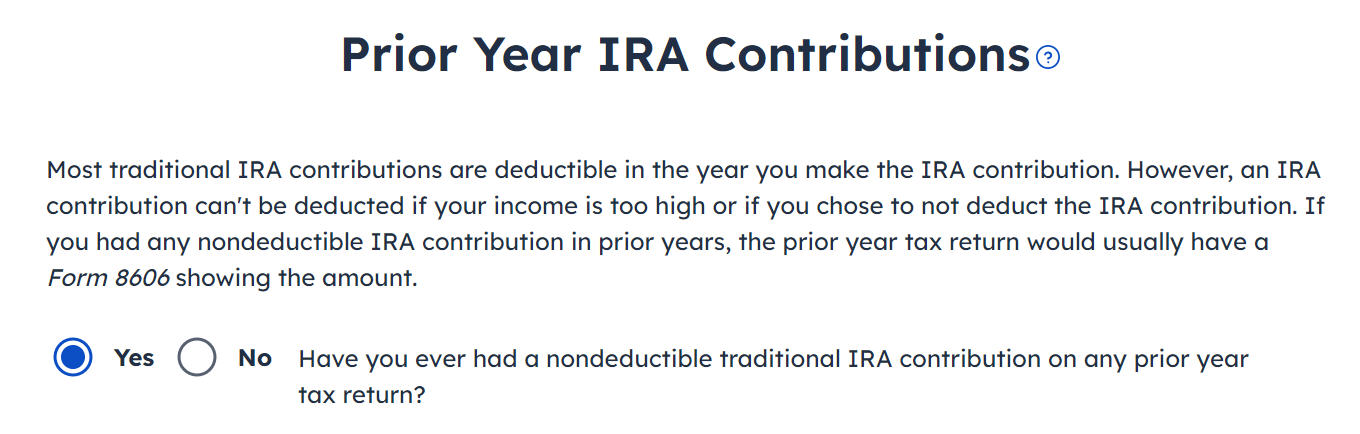

Solution “Sure” right here since you had a Conventional IRA contribution from ultimate 12 months.

Get the price for the primary field from ultimate 12 months’s Shape 8606 Line 14 (assuming that you just did ultimate 12 months accurately). If you happen to didn’t have a Shape 8606 ultimate 12 months since you didn’t do it accurately, your foundation is the volume of your 2022 Conventional IRA contribution minus any deduction you took on ultimate 12 months’s Time table 1 Line 20. The entire foundation is $6,000 in our instance.

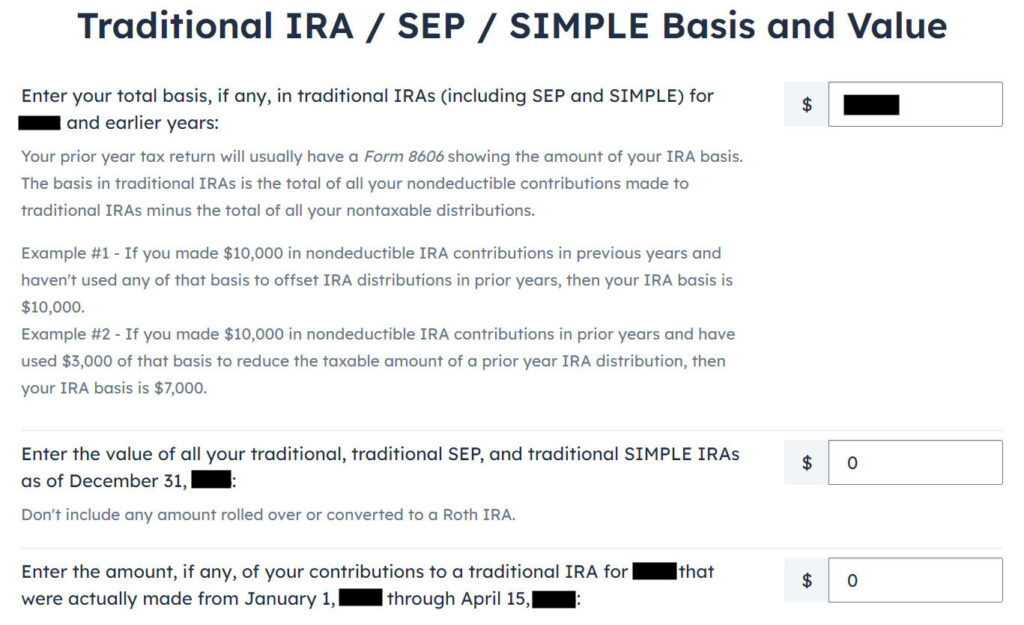

The second one field will have to be 0 whilst you emptied your whole Conventional IRAs after changing them to Roth and also you don’t have any SEP or SIMPLE IRAs. If you happen to had a couple of greenbacks of profits posted within the Conventional IRA after you transformed and also you left them within the account, get the price out of your year-end observation and put it in the second one field. The tool will practice the pro-rata rule.

The 3rd field will have to even be 0 whilst you made your 2023 contribution in 2023.

We didn’t take any crisis distribution.

Now proceed with all different source of revenue pieces till you’re achieved with source of revenue.

Blank Backdoor Roth On Most sensible

If you happen to did a “blank” backdoor Roth on most sensible of changing the 2022 contribution in 2023 (contributed to a Conventional IRA for 2023 in 2023 and transformed in 2023), the conversion a part of the blank backdoor Roth is already integrated within the 1099-R shape we simply finished. Now we do the contribution phase.

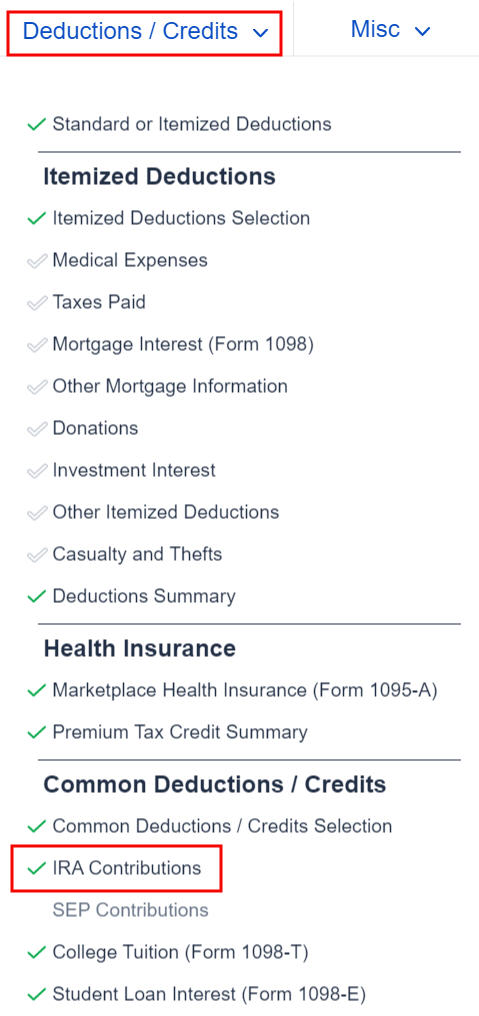

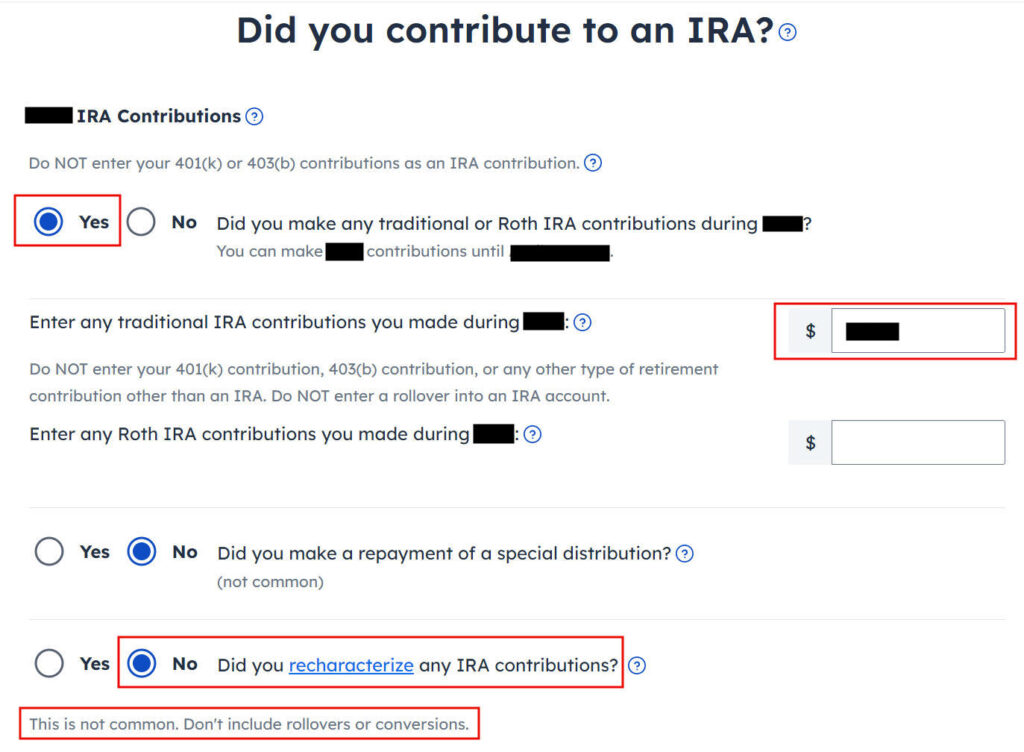

To find the “IRA Contributions” segment below the “Deductions / Credit” menu.

Solution “Sure” to the primary query and input your contribution in your Conventional IRA. Depart the solution to “Did you recharacterize” at No. We contributed $6,500 in our instance.

Your refund quantity is going up once more after you input the contribution.

We didn’t give a contribution to a SEP, SIMPLE, or solo 401k plan on this instance. Solution Sure for those who did.

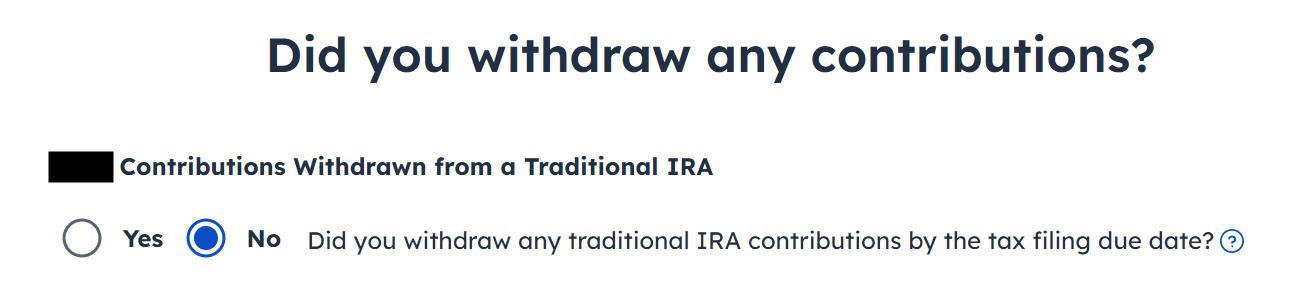

“Withdraw” manner pulling cash out of a Conventional IRA again in your bank account. Changing to Roth isn’t a withdrawal. Solution “No” right here.

FreeTaxUSA displays the similar web page we noticed sooner than within the conversion segment. Ascertain and proceed.

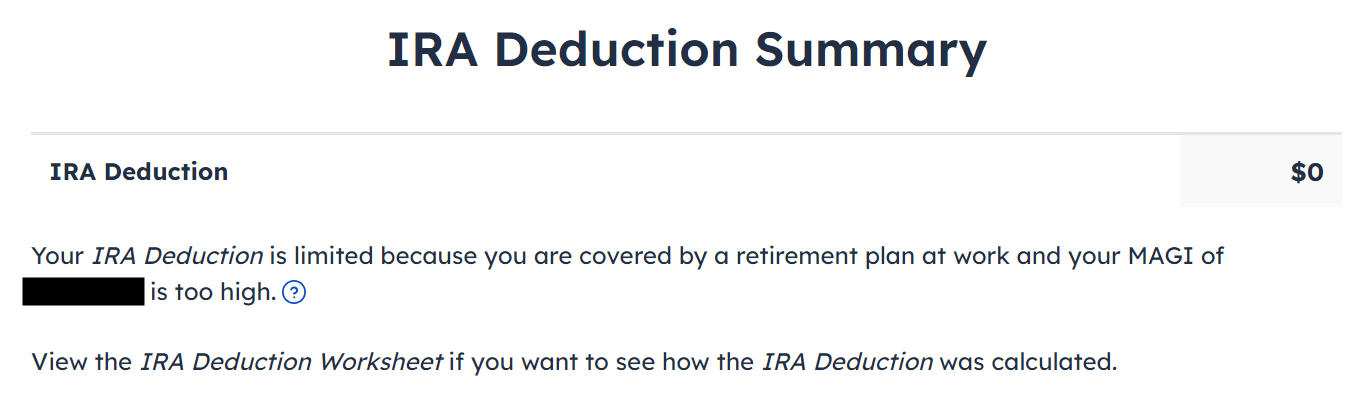

It tells us we don’t get a deduction as a result of our source of revenue is just too top. If you happen to see a deduction right here it manner the tool thinks your source of revenue qualifies for a deduction, which might or will not be proper. Please see the Troubleshooting segment.

Taxable Source of revenue

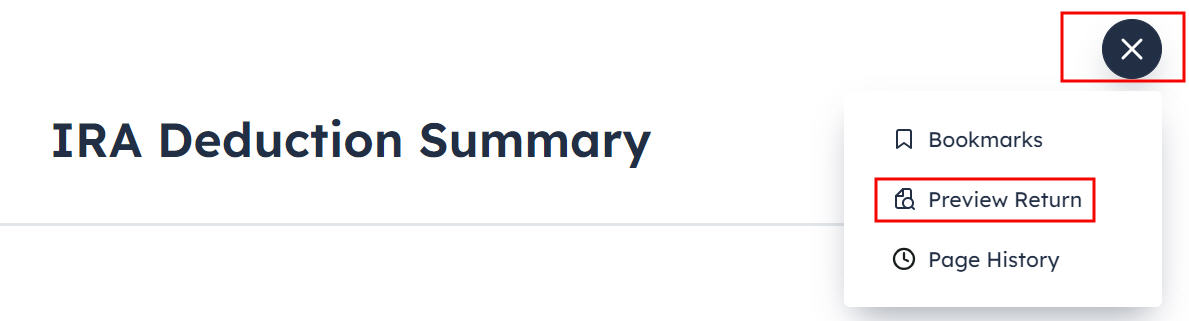

You’re achieved with the 1099-R bureaucracy. Let’s have a look at how they display up in your tax go back. Click on at the 3 dots at the most sensible proper above the IRA Deduction Abstract after which click on on “Preview Go back.”

Search for Strains 4a and 4b for your Shape 1040.

Line 4a displays the volume in your 1099-R for the Roth conversion. Line 4b displays the taxable quantity, which is the profits between the time you contributed in your Conventional IRA and the time you transformed it to Roth. The taxable quantity on Line 4b could be 0 for those who didn’t have any profits.

Move towards the top within the pop-up to search out Shape 8606. It displays those for our instance:

| Line # | Quantity |

|---|---|

| 1 | 6,500 (provided that you additionally did a “blank” backdoor Roth on most sensible, differently clean.) |

| 2 | 6,000 |

| 3 | The sum of Line 1 and Line 2 |

| 5 | The similar as Line 3 |

| 8 | The volume in your 1099-R with a code 2 or 7 |

| 13 | The similar as Line 3 |

| 14 | clean (or a small quantity in case your Conventional IRA had a small steadiness on the finish of 2023) |

| 16 | The similar as Line 8 |

| 17 | Line 3 minus Line 14 |

| 18 | The variation between Line 16 and Line 17 |

Troubleshooting

If you happen to adopted the stairs and also you aren’t getting the anticipated effects, right here are some things to test.

Conversion Is Taxed

If you happen to don’t have a retirement plan at paintings, you may have a better source of revenue prohibit to take a deduction in your Conventional IRA contribution. In case you have a retirement plan at paintings however your source of revenue is low sufficient, you’re additionally eligible for a deduction in your Conventional IRA contribution. FreeTaxUSA will give you the deduction if it sees that your source of revenue qualifies. It doesn’t provide the selection of making it non-deductible.

A part of your conversion might be taxed since you took a deduction at the Conventional IRA contribution ultimate 12 months or this 12 months. You notice whether or not you took a deduction by way of having a look at Time table 1 Line 20 on ultimate 12 months’s and this 12 months’s tax returns.

The taxable Roth IRA conversion and the deduction to your Conventional IRA contribution offset each and every different to create a wash. That is commonplace and it doesn’t reason any issues whilst you certainly don’t have a retirement plan at paintings or when your source of revenue is adequately low.

If you happen to if truth be told have a retirement plan at paintings, possibly the tool didn’t see it. Whether or not you may have a retirement plan at paintings is marked by way of the “Retirement plan” field in Field 13 of your W-2.

Perhaps you forgot the test it whilst you entered the W-2. Double-check the “Retirement plan” field in Field 13 of your (and your partner’s) W-2 entries in FreeTaxUSA to ensure they fit the W-2.

Self vs Partner

If you’re married, remember to don’t have the 1099-R and the IRA contribution blended up between your self and your partner. If you happen to inadvertently assigned two 1099-Rs to at least one particular person as a substitute of 1 for you and one to your partner, the second one 1099-R is not going to fit up with a Conventional IRA contribution made by way of a partner. If you happen to entered a 1099-R for each your self and your partner however you best entered one Conventional IRA contribution, you’re going to be taxed on one 1099-R.

Say No To Control Charges

If you’re paying an consultant a proportion of your property, you’re paying 5-10x an excessive amount of. Discover ways to in finding an impartial consultant, pay for recommendation, and best the recommendation.