2023 2024 2025 Medicare Section B IRMAA Top class MAGI Brackets

[Updated on September 13, 2023 after the release of the inflation number for August 2023.]

Seniors 65 or older can join Medicare. The federal government calls individuals who obtain Medicare beneficiaries. Medicare beneficiaries will have to pay a top rate for Medicare Section B which covers medical doctors’ services and products and Medicare Section D which covers prescribed drugs. The premiums paid by way of Medicare beneficiaries quilt about 25% of this system prices for Section B and Section D. The federal government will pay the opposite 75%.

What Is IRMAA?

Medicare imposes surcharges on higher-income beneficiaries. The speculation is that higher-income beneficiaries can manage to pay for to pay extra for his or her healthcare. As an alternative of doing a 25:75 break up with the federal government, they will have to pay a better proportion of this system prices.

The surcharge is named IRMAA, which stands for Source of revenue-Comparable Per 30 days Adjustment Quantity. This is applicable to each Conventional Medicare (Section B and Section D) and Medicare Benefit plans.

In line with the Medicare Trustees File, 7% of Medicare Section B beneficiaries paid IRMAA. The additional premiums they paid decreased the federal government’s proportion of the entire Section B and Section D bills by way of two proportion issues. Large deal?

MAGI

The revenue used to resolve IRMAA is your Changed Adjusted Gross Source of revenue (MAGI) — which is your AGI plus tax-exempt pastime and dividends from muni bonds — from two years in the past. Your 2021 MAGI determines your IRMAA in 2023. Your 2022 MAGI determines your IRMAA in 2024. Your 2023 MAGI determines your IRMAA in 2025.

There are lots of definitions of MAGI for various functions. The MAGI for subsidies on medical health insurance from the ACA market comprises untaxed Social Safety advantages. The MAGI for IRMAA doesn’t come with untaxed Social Safety advantages. When you learn in other places that claims that untaxed Social Safety advantages are integrated in MAGI, they’re speaking a couple of other MAGI, now not the MAGI for IRMAA.

You’ll use Calculator: How A lot of My Social Safety Advantages Is Taxable? to calculate the taxable portion of your Social Safety advantages.

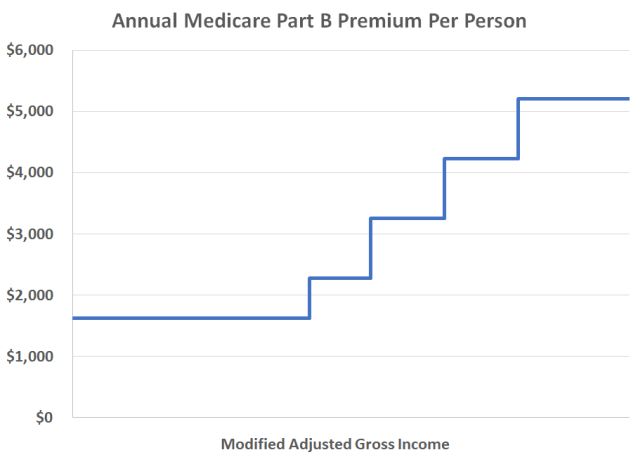

As though it’s now not sophisticated sufficient whilst now not shifting the needle a lot, IRMAA is split into 5 revenue brackets. Relying at the revenue, higher-income beneficiaries pay 35%, 50%, 65%, 80%, or 85% of this system prices as an alternative of 25%. Because of this, they pay 1.4 instances, 2.0 instances, 2.6 instances, 3.2 instances, or 3.4 instances the usual Medicare top rate.

The brink for every bracket may cause a surprising bounce within the per month top rate quantity you pay. In case your revenue crosses over to the following bracket by way of $1, impulsively your Medicare premiums can bounce by way of over $1,000/12 months. If you’re married submitting a joint tax go back and either one of you might be on Medicare, $1 extra in revenue could make the Medicare premiums bounce by way of over $1,000/12 months for every of you.

* The ultimate bracket at the some distance proper isn’t displayed within the chart.

So in case your revenue is close to a bracket cutoff, see if you’ll organize to stay it down and make it keep in a decrease bracket. The use of the revenue from two years in the past makes it harder to control.

2023 IRMAA Brackets

The revenue to your 2021 IRS tax go back (filed in 2022) determines the IRMAA you pay in 2023.

| Section B Top class | 2022 Protection (2020 Source of revenue) | 2023 Protection (2021 Source of revenue) |

|---|---|---|

| Usual | Unmarried: <= $91,000 Married Submitting Collectively: <= $182,000 Married Submitting One after the other <= $91,000 | Unmarried: <= $97,000 Married Submitting Collectively: <= $194,000 Married Submitting One after the other <= $97,000 |

| 1.4x Usual | Unmarried: <= $114,000 Married Submitting Collectively: <= $228,000 | Unmarried: <= $123,000 Married Submitting Collectively: <= $246,000 |

| 2.0x Usual | Unmarried: <= $142,000 Married Submitting Collectively: <= $284,000 | Unmarried: <= $153,000 Married Submitting Collectively: <= $306,000 |

| 2.6x Usual | Unmarried: <= $170,000 Married Submitting Collectively: <= $340,000 | Unmarried: <= $183,000 Married Submitting Collectively: <= $366,000 |

| 3.2x Usual | Unmarried: < $500,000 Married Submitting Collectively: < $750,000 Married Submitting One after the other < $409,000 | Unmarried: < $500,000 Married Submitting Collectively: < $750,000 Married Submitting One after the other < $403,000 |

| 3.4x Usual | Unmarried: >= $500,000 Married Submitting Collectively: >= $750,000 Married Submitting One after the other >= $409,000 | Unmarried: >= $500,000 Married Submitting Collectively: >= $750,000 Married Submitting One after the other >= $403,000 |

Supply: Medicare Prices, Medicare.gov

The usual Section B top rate is $164.90 in 2023.

Upper-income Medicare beneficiaries additionally pay a surcharge for Section D. The revenue brackets are the similar. The Section D IRMAA surcharges are reasonably smaller in greenbacks.

2024 IRMAA Brackets

We have now all 12 knowledge issues out of 12 for the IRMAA brackets in 2024 (in keeping with 2022 revenue). Medicare will make the reputable announcement quickly.

| Section B Top class | 2023 Protection (2021 Source of revenue) | 2024 Protection (2022 Source of revenue) |

|---|---|---|

| Usual | Unmarried: <= $97,000 Married Submitting Collectively: <= $194,000 Married Submitting One after the other <= $97,000 | Unmarried: <= $103,000 Married Submitting Collectively: <= $206,000 Married Submitting One after the other <= $103,000 |

| 1.4x Usual | Unmarried: <= $123,000 Married Submitting Collectively: <= $246,000 | Unmarried: <= $129,000 Married Submitting Collectively: <= $258,000 |

| 2.0x Usual | Unmarried: <= $153,000 Married Submitting Collectively: <= $306,000 | Unmarried: <= $161,000 Married Submitting Collectively: <= $322,000 |

| 2.6x Usual | Unmarried: <= $183,000 Married Submitting Collectively: <= $366,000 | Unmarried: <= $193,000 Married Submitting Collectively: <= $386,000 |

| 3.2x Usual | Unmarried: < $500,000 Married Submitting Collectively: < $750,000 Married Submitting One after the other < $403,000 | Unmarried: < $500,000 Married Submitting Collectively: < $750,000 Married Submitting One after the other < $397,000 |

| 3.4x Usual | Unmarried: >= $500,000 Married Submitting Collectively: >= $750,000 Married Submitting One after the other >= $403,000 | Unmarried: >= $500,000 Married Submitting Collectively: >= $750,000 Married Submitting One after the other >= $397,000 |

I additionally mission the Social Safety COLA and the tax brackets for subsequent 12 months. Please learn 2024 Social Safety Value of Dwelling Adjustment (COLA) Projections and 2024 Tax Brackets, Usual Deduction, Capital Positive aspects, and many others. if you happen to’re .

2025 IRMAA Brackets

We don’t have any knowledge at the moment for the IRMAA brackets in 2025 (in keeping with 2023 revenue). Alternatively, you’ll make some initial estimates and provides your self some margin to stick transparent of the cutoff issues.

If annualized inflation from September 2023 thru August 2024 is 0% (costs staying flat at the newest stage) or 3% (roughly a zero.25% building up each month), those would be the 2025 numbers:

| Section B Top class | 2025 Protection (2023 Source of revenue) 0% Inflation | 2025 Protection (2023 Source of revenue) 3% Inflation |

|---|---|---|

| Usual | Unmarried: <= $105,000 Married Submitting Collectively: <= $210,000 Married Submitting One after the other <= $105,000 | Unmarried: <= $106,000 Married Submitting Collectively: <= $212,000 Married Submitting One after the other <= $106,000 |

| 1.4x Usual | Unmarried: <= $132,000 Married Submitting Collectively: <= $264,000 | Unmarried: <= $134,000 Married Submitting Collectively: <= $268,000 |

| 2.0x Usual | Unmarried: <= $164,000 Married Submitting Collectively: <= $328,000 | Unmarried: <= $167,000 Married Submitting Collectively: <= $334,000 |

| 2.6x Usual | Unmarried: <= $197,000 Married Submitting Collectively: <= $394,000 | Unmarried: <= $200,000 Married Submitting Collectively: <= $400,000 |

| 3.2x Usual | Unmarried: < $500,000 Married Submitting Collectively: < $750,000 Married Submitting One after the other < $395,000 | Unmarried: < $500,000 Married Submitting Collectively: < $750,000 Married Submitting One after the other < $394,000 |

| 3.4x Usual | Unmarried: >= $500,000 Married Submitting Collectively: >= $750,000 Married Submitting One after the other >= $395,000 | Unmarried: >= $500,000 Married Submitting Collectively: >= $750,000 Married Submitting One after the other >= $394,000 |

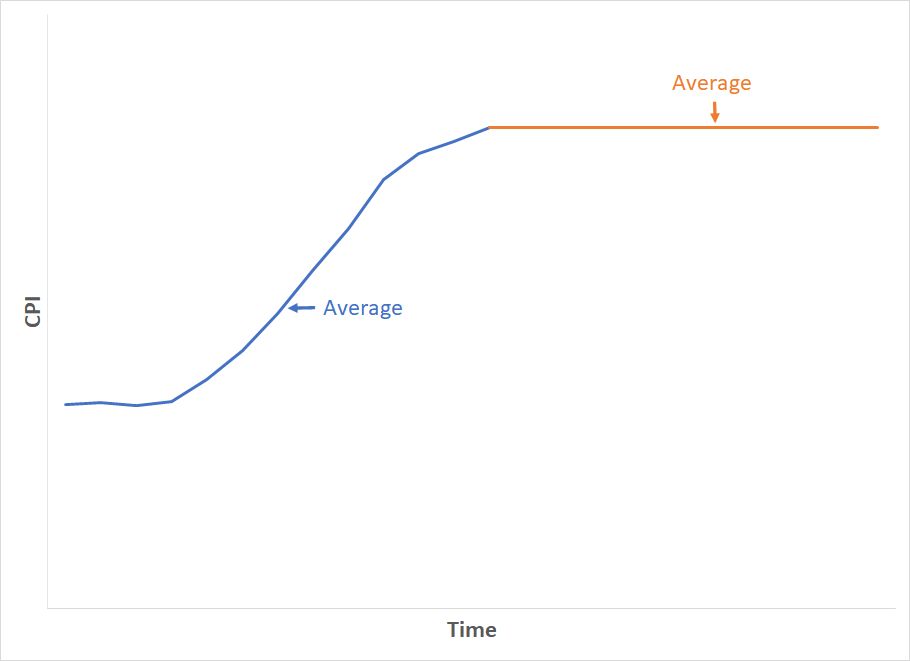

Since the formulation compares the moderate of 12 per month CPI numbers over the moderate of 12 per month CPI numbers in a base duration, although costs keep the similar within the following months, the common of the following one year will nonetheless be larger than the common within the earlier one year. To make use of exaggerated numbers, assume gasoline costs went up from $3/gallon to 4.50/gallon over the past one year. The typical gasoline value within the ultimate 12 numbers used to be perhaps $3.70/gallon. When gasoline value inflation turns into 0%, it method it remains at $4.50/gallon. The typical for the following one year is $4.50/gallon. Brackets in keeping with a mean gasoline value of $4.50/gallon shall be larger than brackets in keeping with a mean gasoline value of $3.70/gallon.

When you in point of fact need to get into the weeds of the technique for those calculations, please learn remark #79 and remark #164.

Nickel and Dime

The usual Medicare Section B top rate is $164.90/month in 2023. A 40% surcharge at the Medicare Section B top rate is ready $800/12 months in line with individual or about $1,600/12 months for a married couple each on Medicare.

Within the grand scheme, when a pair on Medicare has over $194,000 in revenue, they’re already paying a great amount in taxes. Does making them pay some other $1,600 make that a lot distinction? It’s not up to 1% in their revenue however nickel-and-diming simply makes other folks mad. Folks stuck by way of wonder when their revenue crosses over to a better bracket by way of only a small quantity are offended on the executive. Rolling all of it into the revenue tax could be a lot more efficient.

Oh neatly, in case you are on Medicare, watch your revenue and don’t by accident move a line for IRMAA.

IRMAA Attraction

In case your revenue two years in the past used to be larger since you have been operating at the moment and now your revenue is considerably decrease since you retired (“paintings aid” or “paintings stoppage”), you’ll enchantment the IRMAA preliminary choice. The “life-changing occasions” that make you eligible for an enchantment come with:

- Demise of partner

- Marriage

- Divorce or annulment

- Paintings aid

- Paintings stoppage

- Lack of revenue from revenue generating assets

- Loss or aid of positive varieties of pension revenue

You record an enchantment with the Social Safety Management by way of filling out the shape SSA-44 to turn that despite the fact that your revenue used to be larger two years in the past, you had a discount in revenue now because of one of the most life-changing occasions above. For more info at the enchantment, see Medicare Section B Top class Appeals.

Now not Penalized For Existence

In case your revenue two years in the past used to be larger and also you don’t have a life-changing match that makes you qualify for an enchantment, you’re going to pay the upper Medicare premiums for twelve months. IRMAA is re-evaluated yearly as your revenue adjustments. In case your larger revenue two years in the past used to be because of a one-time match, reminiscent of understanding capital positive aspects or taking a big withdrawal out of your IRA, when your revenue comes down within the following 12 months, your IRMAA will even come down routinely. It’s now not the tip of the sector to pay IRMAA for twelve months.

While you organize your revenue by way of doing Roth conversions, you will have to watch your MAGI moderately to steer clear of by accident crossing such a IRMAA thresholds by way of a small quantity and triggering larger Medicare premiums.

I exploit two equipment to lend a hand with calculating how a lot to transform to Roth. I wrote about those equipment in Roth Conversion with Social Safety and Medicare IRMAA and Roth Conversion with TurboTax What-If Worksheet.

Say No To Control Charges

If you’re paying an guide a proportion of your property, you might be paying 5-10x an excessive amount of. Learn to in finding an unbiased guide, pay for recommendation, and handiest the recommendation.